This week's HEADLINES

Good afternoon Fellow Members,

What a great race here over the weekend for the Gold Coast 600 with plenty of action on the Saturday with continuos rain most of the day. Ford's Scott McLaughlin has pulled off a remarkable Supercars comeback win on the streets of Surfers Paradise as this year's nail-biting championship race gets even tighter.

McLaughlin pitted a lap before his championship rivals, coming out in front of both once all three cars had completed their compulsory second stop in Sunday's 300-kilometre race on the Gold Coast.

The 24-year-old then kept his nose clear of the Holden pair to secure the win before running out of fuel on his victory lap and being forced to push his car back to the pit.

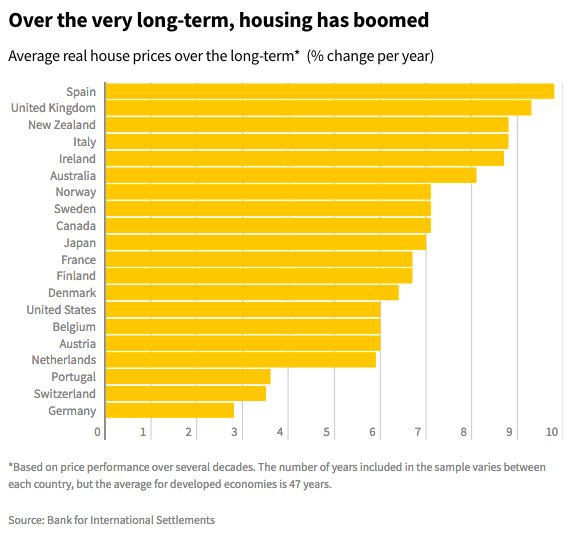

How Australia's Housing Economy compares across 47 Countries

The long-term rise in Australian house prices since the early 1960s has been the most sustained property market upswing in the world in recent decades, new research says. Researchers at the Switzerland-based Bank for International Settlements have analysed long-run trends in house prices across 47 countries, as part of a paper exploring how interest rates affect the price of real estate.

The paper, which finds short-term interest rates are a "surprisingly important" driver of house prices, also includes extensive data that underline the sheer size of the boom in house prices here and elsewhere. In one such illustration, the authors analyse housing market "upswings" and "downswings" - which they define as periods of price rises (or falls) that last for three years or more.

The report found upswings had been far more common than downswings across the 47 countries, accounting for nearly 80 per cent of the periods studied in advanced economies. The long-term rise in Australian housing was the most persistent of all. "The upswings lasted on average 13 years; with the longest one, in Australia, still continuing after half a century," the report said. "By contrast, downswings accounted for only 8 per cent of the advanced economy sample; they lasted on average five years, and the longest one, in Japan, lasted 13 years."

From 1961 to 2016, the report says Australian house prices have grown by an average of 8.1 per cent a year, in "nominal" terms - not taking account of inflation. That is the sixth-highest growth rate among developed nations. Since 1961, it says the cumulative gain in Australian property prices is a whopping 6556 per cent.

That compares with a cumulative 1332 per cent, or 13-fold, rise in United States house prices over 47 years. Australia's nominal cumulative growth is lower than the 7726 per cent increase in Norway's housing market, although that occurred over a longer timeframe of 66 years.

In "real" or inflation-adjusted terms, Australian prices have risen by an average of 3 per cent a year since 1961, with cumulative gains of 373 per cent. The authors acknowledge their data is "unbalanced", as it spans different periods of time depending on the country.

Even so, it highlights very strong growth in property prices over multiple decades. "Is housing a good long-term investment? Our data suggest that the answer is an unqualified "yes": real house prices increased on average by close to 7 per cent per annum in the sample of 20 advanced economies for which there are 45 years of data on average," said the working paper, by Gregory Sutton, Dubravko Mihaljek and Agne Subelyte.

Given the study's focus on national prices, and long-term moves, it does not consider localised falls in house prices within Australian cities, or falls that lasted less than three years. By the author's definitions, Switzerland, Sweden, Canada and New Zealand have also not experienced a "downswing" of three years or more in their house prices.

However, the data the researchers used for these countries do not go back as far in time as Australia's figures, giving Australia the longest-running "upswing". The research comes as Australian regulators and central banks are keenly focused on the risks created by a build-up of housing debt, which has reached record highs after the growth spurt of recent years.

The Reserve Bank last week warned about several areas where it sees "potential risk" in the property investment market, such as the growing number of people with multiple investment properties, and an increase in investors aged over 60 who have a mortgage.

A key finding of the BIS report is that there is a lag between changes in interest rates and movements in house prices, and it can take up to five years for changes in borrowing costs to have a major impact on prices. T

he authors said this delayed response might be because of the high "transaction costs" (such as taxes and real estate fees) involved in property purchases. Correction: An earlier version of this story said Australian house prices had risen by an average of 8.1 per cent a year between 1961 and 2016 in "real" or inflation-adjusted terms.

That reflected an error in the BIS paper, which has been corrected. The story has also been corrected to say this increase was "nominal," meaning it did not take inflation into account.

Have an enjoyable week ahead as we continue to deliver the latest NEWS & REVIEWS in the world of The FIRM :)

In the mean-time stay HEALTHY, WEALTHY & WISE.

Good afternoon Fellow Members,

In case you were not aware we have a Public Holiday, Queens Birthday celebrations today so this will answer your questions why no offices are woking today except The FIRM. :)

Finally, we had a good saturation of rain yesterday with predicted overcast for the rest of the week which is a welcome change from almost drought conditions here on the Gold Coast.

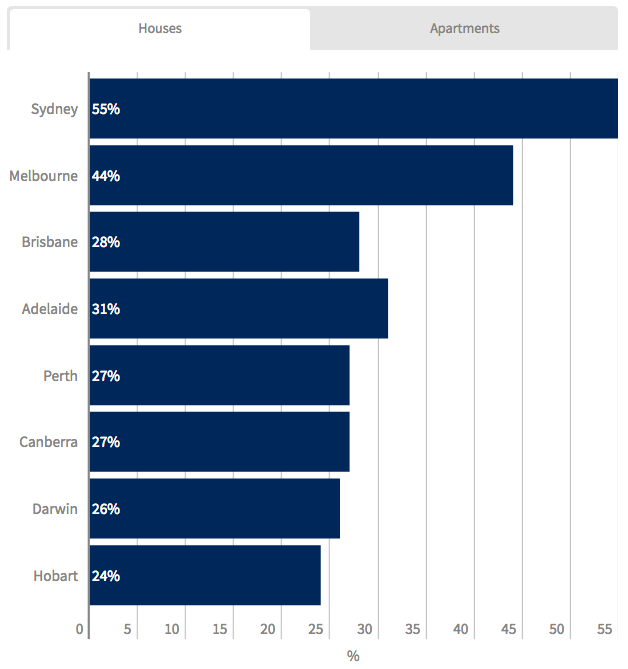

Households in four of Australia's capital cities need six-figure incomes to afford a median-priced house without feeling the pinch, a new analysis shows.

Buyers in Sydney would need to make more than $190,000 a year to avoid spending more than 30 per cent of their income on mortgage repayments, a RateCity analysis found. This is almost $90,000 more than the current average income, and assumes they have $235,000 to cover a 20 per cent deposit on a median-priced home.

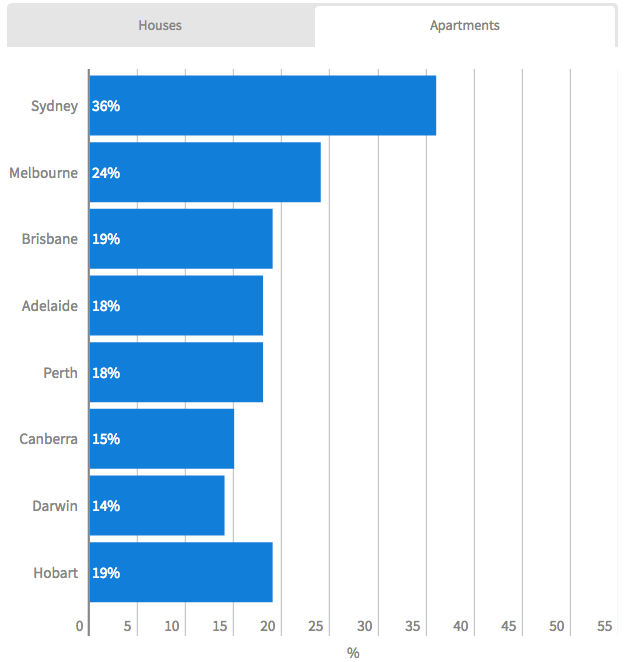

To buy a median-priced apartment apartment, they would need to earn $122,900. In Melbourne, household earnings would need to be above $140,000 for a house and $77,000 for an apartment. Six-figure salaries were also needed to buy a median-priced house in Canberra and Darwin.

The current average annual household incomes in Sydney and Melbourne are about $100,000 and $95,000 respectively.

Note: Calculations are based on owner-occupier paying principal and interest over 30 years with a 20 per cent deposit, on a discounted variable rate with one of the major banks, as reported by the RBA for May 2017. Average house & apartment prices are from Domain State of the Market Report, June 2017. Average income based on 2016 Census data median weekly household income. Source: RateCity

The figures are a stark illustration of "how dire the situation has become in Sydney for a generation of first home buyers",

RateCity spokeswoman Sally Tindall said. "Earning over $100,000 used to be considered wealthy, but in Sydney's real estate market you can't even afford a basic unit without going into mortgage stress," she said. Related: 'Perfect storm of issues' on verge of mortgage crisis Related: Three charts on Australian mortgage stress Related: Reserve Bank and APRA pave way for debt stress "Buying a house in Melbourne is also tough for first home buyers.

However, apartment prices are still reasonable and affordable for those looking to break into the market." While house prices have more than doubled in Sydney since 2008, and almost reached this level in Melbourne, the national weekly income has increased by $27 in the same time period. University of Sydney senior lecturer Dallas Rogers said the household income figure required to buy a median priced home was "alarming". He warned mortgage stress wasn't solely due to individual choices made by households but also due to lenders and the broader property industry.

"What this means for affordable housing and financial policy is that we need to do more than trying to get households to rein in their mortgage and household spending," Dr Rogers said. "We need policy to rein in the financial, mortgage, property development, and real estate sectors to change the structural dynamics that put people in mortgage stress."

But University of NSW City Futures Research Centre research fellow Chris Martin said caution needed to be exercised with these measures of affordability as those entering the market wouldn't necessarily be buying median-priced homes.

Simply, many buyers of mid-priced properties would be "upgraders" using equity from their current home to buy at this price level which would reduce their mortgage costs. And those who earn higher incomes would, of course, be able to afford a higher percentage of their pay taken up on repayments. Despite this, and low interest rates keeping many home buyers' repayments low, "Australian households are among the most indebted in the world, and it is hard to see how servicing costs can get very much lower than at present", Dr Martin said. "Interest rates may rise and even if they don't, repayments may rise if banks start getting serious about making interest-only borrowers start to pay back loan principal too."

Already, some researchers are recording an increase in mortgage stress. Ratings agency Moody's has found home loan arrears where borrowers are behind in repayments has reached a five-year high. Roy Morgan found 17.3 per cent of borrowers in July 2017 were in this category, up 0.3 per cent over the year despite declining interest rates for home loans. And the proportion who were "extremely at risk" increased from 12.4 per cent to 12.8 per cent in the 12-month period. Roy Morgan Research's industry communications director Norman Morris said nearly one in six borrowers faced a potential problem, which would be exacerbated when rates rise. "[This] is likely to lead to an even lower number of borrowers but existing mortgage holders who have borrowed in a low-interest-rate environment are likely to face increased levels of mortgage stress," Mr Morris said. "The final impact, however, will also be determined by what happens to household incomes, which are currently showing very modest growth."

Simply, many buyers of mid-priced properties would be "upgraders" using equity from their current home to buy at this price level which would reduce their mortgage costs. And those who earn higher incomes would, of course, be able to afford a higher percentage of their pay taken up on repayments.

Despite this, and low interest rates keeping many home buyers' repayments low, "Australian households are among the most indebted in the world, and it is hard to see how servicing costs can get very much lower than at present", Dr Martin said. "Interest rates may rise and even if they don't, repayments may rise if banks start getting serious about making interest-only borrowers start to pay back loan principal too." Already, some researchers are recording an increase in mortgage stress. Ratings agency Moody's has found home loan arrears where borrowers are behind in repayments has reached a five-year high. Roy Morgan found 17.3 per cent of borrowers in July 2017 were in this category, up 0.3 per cent over the year despite declining interest rates for home loans. And the proportion who were "extremely at risk" increased from 12.4 per cent to 12.8 per cent in the 12-month period.

Roy Morgan Research's industry communications director Norman Morris said nearly one in six borrowers faced a potential problem, which would be exacerbated when rates rise. "[This] is likely to lead to an even lower number of borrowers but existing mortgage holders who have borrowed in a low-interest-rate environment are likely to face increased levels of mortgage stress," Mr Morris said. "The final impact, however, will also be determined by what happens to household incomes, which are currently showing very modest growth."

Mortgage Choice chief executive John Flavell said there was no denying the expensive nature of Sydney property. "The best thing borrowers can do to ensure they don't find themselves in mortgage stress in the future if and when rates rise, is not stretch themselves too thin," Mr Flavell said. He recommended borrowers review their finances regularly.

So give us a call NOW for a Financial Tune Up to ensure you are on track! I

n the mean-time stay HEALTHY, WEALTHY & WISE.

A $3 billion "integrated resort" casino development planned for the Gold Coast Spit has been rejected.

Good afternoon Fellow members,

THE Queensland Government has terminated a planned multi-billion dollar resort and casino on the Gold Coast, saying that there needs to be a balance between environmental and commercial concerns.

The resort, which had the backing of Chinese company ASF, was to have been built on Crown land on the Spit at Southport with a five tower integrated complex including a casino.

Queensland Premier Annastacia Palaszczuk says the decision is based on ensuring the "best long-term solution" for the Gold Coast, and says the Government will move forward with a community-led master plan. "Like many Queenslanders, I have enjoyed visiting the Spit for decades," Ms Palaszczuk says. "We need to ensure that character is preserved for future generations.

The Spit offers great opportunities for job creation through tourism, entertainment and recreation. "What the Spit really needs now is a master plan to revitalise it and increase its benefit to the Gold Coast as a community asset." "To be clear, this is not a decision that rules out a future Integrated Resort Development on the Gold Coast."

The Government says the new master plan will ensure the Spit remains a low-density area with a maximum three storey limit to apply to any redevelopment. It is expected the master plan will take 18 months to complete. It's believed that the decision will not affect moves by Gold Coast Mayor Tom Tate to push for construction of a cruise ship terminal in the area.

Chat to you soon!

Gold Coast - Beyond the Horizon

Beyond the Horizon of the Gold Coast. Sixth largest city on the Australian continent. Non-existent at the time of the 1954 census but today a metropolis of more than 600,000 residents. By the middle of the century the Coast will still be this nation's sixth largest city but it will also be a city of truly metropolitan scale. What will the Gold Coast look like in 2050?

Beyond the Horizon paints a picture of what this truly remarkable city will look like. This 33 page report explains why! Click Here to download.

More information at https://futuregoldcoast.com.au/

Our Property Manager Retires

As you are all aware our previous Head of our Property Management Team has retired and we have been researching other management businesses to fill the gap.

We have been constantly on the alert looking for someone who can take over the role. We are in final negotiations now with a very exciting, new age format that is keeping up with the times yet still maintaining our good old fashion service of excellence. It will not be too long before the decision will be made to fill this very important role for the future.

In the meantime business as usual with the rest of our team are at your disposal. If your On-Site Management is not performing to your expectations then give us a call.

Clampdown on interest only loans

Interest Rates remain stable 'The tough new rules announced by the Australian Prudential Regulation Authority yesterday which will limit higher-risk, interest-only lending to 30 per cent of all new residential mortgages and require strict controls on interest-only loans with deposits smaller than 20 per cent.'

Response:

Over 95% of our clients do contribute a deposit of 20% or more to their investment purchase so would be largely unaffected by this.

Also - interest only loans are the most lucrative loan structure for banks so no doubt they will finds ways to circumvent this new APRA ruling in their quest to continually deliver great profits / returns to their shareholders.

Stamp duty rules in Victoria to change from July 1st.

After July 1st, 2017, there will no longer be stamp duty discounts offered to off-plan purchases in Victoria.

Response:

Victoria is the last state to offer these discounts so it is somewhat surprising that the Government & State Revenue Office have taken this long to wake up to that significant amount of lost potential tax revenue. Most developers are still going to require 'pre-sales' to qualify for construction funding to enable their project to 'get underway'. Most banks have increased the 'pre-sale requirement' imposed on developers over the last 12-18 months.

The developers we have spoken to and the industry in general will respond by offering their own financial incentive to buyers that commit at the early 'off plan stage' of their projects which will effectively be a substitute for the loss of government stamp duty incentive. This means that those developers will have to factor these financial incentives into the financial feasibility of a projects which may mean that a project that was previously viable will no longer be.'c'est la vie'.

Having said all of that if you have a chance of buying before June 30th.DO IT!

Property Market Bubble in Melbourne and Sydney

Response:

Melbourne is a city made up of hundreds of suburbs, it is therefore erroneous to talk about Melbourne as a single market.

In a similar context, there are many companies that make up the ASX some are overpriced and heading south whilst others no doubt represent great investments (if anyone knows this share market secret please do tell!!)

Similar to the sharemarket, there are certain pockets / suburbs in Melbourne that: have had crazy growth that we believe is unsustainable. are oversupplied with apartments or 'new house and land packages' are currently undergoing 'gentrification', enjoying other infrastructure benefits, or other factors that are driving demand, with relatively low levels of ongoing supply In summary we believe, as always, that solid research and unemotional buying that is driven by solid data and research is critical and will avoid oversupplied and overheated market segments.

FIRST HOME OWNERS GRANT 52 DAYS to GO!!!!

REMINDER:

Don't forget First HOME OWNERS GRANT (FHOG) for QUEENSLAND has only 52 DAYS to GO before it closes.

If you are seriously considering the FHOG before the 30th June then please do not hesitate to contact me direct as we have some very willing developers and Lenders who are prepared to offer assistance where they can to help you in to your first home .

Okay, that is a overview wrap for this month and we look forward to your call.

BREAKING NEWS!!!!

Don't Miss the Greatest Business Event of the Year

Good afternoon fellow members,

As you may recall last June I attended the Charis Business Summit in Colorado USA.

I'm happy to announce that the Business Summit is coming to Australia in March this year. I learned so much from this conference meeting and made such great Business connections from all around the world. I highly recommend that you attend.

The guest speakers have all taken companies to multi-million dollar levels while walking in integrity and applying Biblical principles. These men started Charis Business School in Colorado and they still teach there today. They are leaders in both the business and spiritual realm. They want to teach you how to maximize your financial life!

Please watch the video in this email and browse through all the information about the Charis Business Summit being held at SeaWorld Convention Centre. Seating is limited to only 450 people so please register as soon as possible.

The Charis Business Summit, located on the beautiful Gold Coast of Australia, consists of 4 power-packed days taught by the leading Christian business minds of our time.

Our 3 world-class guest speakers will teach you how to:

- Create organisational structures that encourage growth and expansion.

- Develop team models that build leaders and promote cross communication.

- Establish business systems and practices that will launch your business or ministry to the next level.

All of which, you'll be able to implement immediately upon completion of this conference.

EVENT DETAILS

The Charis Business Summit will be held on 30 March - 02 April 2017

SeaWorld Resort Conference Centre, Gold Coast.

Your registration includes:

- 4 Powerful Days of Strategic Business and Ministry Development

- Breakout Training Workshops

- Interactive Q & A Sessions

- Complimentary Wi-Fi (rooms & conference centre)

- Morning Tea, Lunch & Afternoon Tea Provided

- Discounted Access to 3 Gold Coast Theme Parks

- Special Discounted Hotel Rooms Available at Sea World Resort; Discount extended 3 Days Prior to & 3 Days After the Conference

GUEST SPEAKERS

Build kingdom wealth with these cutting-edge, business experts:

- Dr. Dean Radtke - Founder and CEO of The Institute of Ministry Management & Leadership.

- Paul Milligan - CEO of AWMI and Director of Charis Business School

- Billy Epperhart - Founder of Tricord Global and WealthBuilders.

![]()

I look forward to personally see you here on March 30th for an action packed and stimulating conference that you will never forget.

Book NOW and take advantage of the EARLY BIRD DISCOUNT.

If you require any additional information please do not hesitate to contact me direct.

Have a great AUSTRALIA DAY celebrations and chat to you soon! In the meantime stay HEALTHY WEALTHY & WISE!