2019 NEWS HEADLINES

LATEST STATISTICS

NATIONALLY:

Sydney's current median price is $780,672

Melbourne's current median price is $621,759

Brisbane's current median price is $484,047

Byron Bay is now officially Australia's most expensive place to buy a house AT $987,00

Sydney's current rental yield is 3.85%

Melbourne's current rental yield is 3.80%

Brisbane's current rental yield is 4.68%

source: Core Logic

POPULATION GROWTH BY STATE:

Sydney population growth 1.5%

Melbourne population growth 2.2%

Brisbane's now passes Sydney with annual population growth of 1.7%

MORE PEOPLE. MORE HOMES.

Source ABS published March 2019

Brisbane Cruise Terminal Set to Welcome One Million Passengers

Good morning fellow members,

Great news as it is all official today that Brisbane Cruise Ship Terminal turned their first sod of soil today.

Completion expected October 2020 which is perfect timing as AQUA SAPPHIRE arrives for the first time in Australia.

Brisbane's first cruise ship terminal is underway, with premier Annastacia Palaszczuk turning the sod on the $158 million project on Tuesday.

The long-awaited terminal is scheduled to open in October 2020, with bookings already open for Brisbane's first cruise season.

Publicised as a significant economic boost for Queensland's tourism industry, the premier said that the terminal will eventually host more than a million passengers each year.

"Building this one piece of infrastructure flows through our entire economy.

"Ships that were too long, too high and too deep to dock at Brisbane's Hamilton facility will have a dedicated cruise terminal."

Deloitte's latest business outlook shows strong population growth numbers bolstering Queensland's economy as "crazy" house prices send buyers north. Tourism numbers are also looking positive, with an expected economic upswing coming from tourism and mining.

"The renewed (albeit modest) falls in the Australian dollar over the past year augur well for renewed strength in tourism numbers ahead," Deloitte partner Chris Richardson said.

"That will be accommodated by the recent increased and ongoing investment in hotel capacity in some of the tourism hubs of the state."

The terminal is expected to handle over 1,100 vessels and at 1.8 million passengers.

Tourism minister Kate Jones said that Queensland's cruise industry was booming.

"Last financial year we saw 520 ships port in Queensland 11% growth year-on-year, making the Sunshine State Australia's undisputed cruise capital."

The terminal is expected to handle over 1,100 vessels and at 1.8 million passengers within its first five years.

The global cruise ship industry is growing, with at least 60% of the cruise ships calling into Australia by 2020 estimated to be "mega" cruise ships with a gross tonnage larger than 120,000.

The Queensland government has confirmed that construction company Hindmarsh will deliver the $158 million building.

The Australian Taxation Office will be targeting real estate investors who are incorrectly calculating taxes on their returns.

Chris Jordan, commissioner of the Australian Taxation Office (ATO), said they recently performed 300 audits on real estate investors and found that almost 9 out of 10 returns contained errors.

In a speech yesterday in Hobart, he said this is a problem.

"We're seeing incorrect interest claims for the entire investment loan where it has been refinanced for private purposes, incorrect classification of capital works as repairs and maintenance, and taxpayers not apportioning deductions for holiday homes when they are not genuinely available for rent."

More than 2.1 million Australians are property investors, who collectively claim more than $47 billion in deductions every year.

But rental income is only $44.1 billion. Mr Jordan believes something is obviously amiss.

"You can get a sense of the potential revenue at risk. A lot of people are getting things a little bit wrong, which adds up to a lot."

Mr Jordan said that after their close examination of work expenses earlier in the year, real estate investment would be their next big focus.

That earlier crackdown resulted in a decrease in average deduction claims for the first time in almost 25 years.

According to Mr Jordan, "The estimated revenue gain for [the last 2 years] will be around $600 million."

That is for the work expenses. It is possible the real estate deductions will turn out to be an even larger matter.

"For those who are antagonistic towards us, and our reform program, who do not want to pay their share of tax, who see the ATO as something of an enemy, I believe community sentiment is against you and will increasingly become more so."

Just something to keep in mind for June 30th.

Treasury Rebukes Coalition for Exaggerating Impact of Negative Gearing Reforms

Courtesy The Urban Developer

Federal Treasury has delivered a serious rebuke to the Coalition for exaggerating the impact of Labor's negative gearing and capital gains changes.

In emails released under freedom of information, acting treasurer Kelly O'Dwyer requested the department fact check the Coalition's claims that Labor's policies would cause house prices to fall.

In response, Treasury issued a correction: "The [s]tatement is not consistent with our advice."

"We did not say that the proposed policies 'will' reduce house prices," the email reads.

"We said that they 'could' put downward pressure on house prices in the short-term depending on what else was going on in the market at the time.

"But in the long-term they were unlikely to have much impact."

Labor has jumped on the release, with shadow treasurer Chris Bowen saying that the government had been "caught red-handed" misrepresenting Treasury's advice.

For his part, treasurer Josh Frydenberg denied that the government was misrepresenting Treasury, pointing to the Financial Review's take on the release that changes "could" put downward pressure on house prices in the short term.

Frydenberg quoted building industry group the Masters Builders Association figures.

"If Labor's policy is in place you'll see 32,000 fewer jobs and 42,000 fewer homes being built."

.

.

Despite the public scolding, treasurer Josh Frydenberg denied that the government misrepresented Treasury's advice.

House prices hit spending

It has been a difficult week in economic policy, with GDP figures released on Wednesday revealing that the economy has slowed significantly, entering a "per capita recession" for the first time in 13 years.

Retail trade figures for the March quarter were also sluggish, with falling house prices impacting wealth and spending.

RBA governor Philip Lowe highlighted the link between the two at the AFR annual business summit on Wednesday.

"The evidence is that a tightening in credit supply has contributed to the slowdown in credit growth," Lowe said.

"The main story, though, is one of reduced demand for credit, rather than reduced supply.

"When housing prices are falling, investors are less likely to enter the market and to borrow. So too are owner-occupiers for a while."

The Australian Suburbs Where Property Prices Fell

Australia recorded 1473 suburbs that declined in value

for the 12 months to November 2018, finds a new report.

LOST PROPERTY

The annual Suburbanite negative growth report, which uses data collected from Corelogic and SQM research, says this is a 37 per cent increase on the year prior.

"When oversupply meets a cooling market, coupled with strained infrastructure, this results in a market seeing downturn, even if the markets surrounding them are not in the same boat yet," Suburbanite founder Anna Porter said.

"One or two of these ingredients may not push a market into negative growth, but when all three fundamental issues collide the market is going to push through pain before the surrounding areas do."

Related: These Are Sydney's Most Affordable Suburbs

Australia recorded 1473 suburbs that declined in value for the 12 months to November 2018.

New South Wales

Data shows the largest falls for houses were recorded in northern beaches suburb Church Point, falling 25.3 per cent. While the largest falls for units were recorded in Mangerton Wollongong recording falls of 43.9 per cent.

Porter said there has been an overdevelopment of units in Ultimo, as a result the unit market in the suburb recorded declines of 29.1 per cent according to the report.

"Ultimo just has too much supply for the market of inappropriate unit stock," Porter said.

"Which just isn't being taken up at the rate it needs to be to accelerate growth."

While positive growth has been projected for the Hills district in Sydney, particularly due to the completion of the new public transport hub, Porter says this achieved no real uplift in the housing prices for many of the Hills district suburbs.

"Winston Hills housing market has declined by 7.5 per cent, North Rocks with 6.9 per cent declines, Kings Langley witnessing 2.6 per cent declines, Cherrybrook seeing 1.2 per cent negative growth, Bella Vista declining by 2.4 per cent and Baulkham Hills declined 2.6 per cent,"

"The prestige pocket housing market of Galston, in the Hills district, has seen a 22.6 per cent decline.

"Prestige rural and residential locations tend to get hit first when the market starts to cool off. Especially when they offer lifestyle properties that have a limited market," Porter said.

Related: What to Expect from the Property Market in 2019: Experts Weigh In

Trendy suburb St Kilda, which sits seven kilometres from Melbourne CBD, suffered the biggest fall for housing.

Victoria

The most negative housing growth recorded in Melbourne was controversially seen in trendy inner suburb St Kilda dropping 28.7 per cent for the period.

Other poor performing housing markets were Cardigan Village (-16.7 per cent), Glenrowan (-16.1 per cent), Lake Wendouree (-19.7 per cent) and Williamstown North (-21.7 per cent).

For units Porter said Melbourne's Aberfeldie reported a 35.8 per cent decline in values, Toorak fell 17.2 per cent, and Blackburn dropping 19.9 per cent.

"The worst performing of the 153 unit market's was Aberfeldie in Melbourne's north-west, nine kilometres from the CBD with a contraction of 35.8 per cent.

"This is a direct outcome of the staggering oversupply of unit stock in these locations, and the CBD as whole, given Melbourne CBD has a unit decline of three per cent itself," Porter said.

"The great news for Victorian investors is that most of the worst performing markets were in remote and rural locations. Places that investors are unlikely to be looking anyway."

Related: These Are Brisbane's Most Affordable Suburbs: Domain

Mount Isa suburb Sunset recorded a drop of 27.9 per cent for the period.

Queensland

While less impact has been seen in Queensland's metro housing market, Porter says its unit and regional markets are certainly feeling the pinch.

The largest housing falls for the state was, perhaps unsurprisingly, recorded in the mining region Mount Isa' suburb of Sunset experiencing a drop of 27.9 per cent.

"A direct reflection of businesses in the area continuing to wind down," she said.

While for units, Beachmere near Deception Bay recorded falls of 49.8 per cent.

Related: Australia's Worst Property Markets Revealed

Western Australia

While Western Australia is starting to recover overall, Porter says there are fewer metro suburbs on the list this year compared to last.

Regional mining towns however are still taking time to stabilise.

"Regional mining towns are great when there's a mining boom, but if you go regional, you have to think what happens when the market turns that corner."

Kambalda West recorded the largest falls for houses, down 35.9 per cent.

While West Busselton dropped by 31.6 per cent for units.

Bucking the trend, South Australia is seeing solid growth, but Porter says it's the regional pockets "still feeling the pain."

Biggest falls for housing in South Australia was Port Macdonnell recording a fall of 22.8 per cent.

And Allenby Gardens which dropped by 28.7 per cent for units.

Tasmania's biggest falls in the housing market was recorded in Shorewell Park Houses dropping by 26.9 per cent.

While for units East Launceston suffered falls of 14.2 per cent.

The political powerhouse of Australia is currently in a growth market, according to Porter, with the Australian Capital Territory mostly experiencing growth.

The exception is the unit market, which "is certainly feeling the pain" with an oversupplied pipeline.

Suburb Mawson saw the largest falls for houses, recording an 8.7 per cent decline.

In the unit market it was the suburb of Phillip which recorded falls of 26.4 per cent.

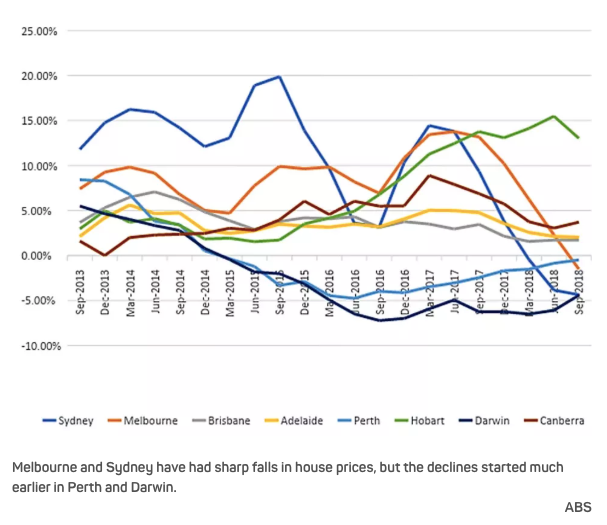

Housing Prices are falling in Sydney and Melbourne,

so Housing must become more affordable ...Right?

The annual growth of house prices has been slowing consistently for more than a year in Australia's largest cities.

Prices finally started falling in the latter part of last year. The decline began much earlier in Perth and Darwin. Prices in most other cities, with the exception of Hobart, have been more stable.

House owners have a secret weapon

A rise in house prices is a mixed blessing. For those whose employment and savings strategies have helped them become home owners, price inflation is a good thing the value of the house rises while the mortgage debt stays the same, or falls.

For others, the savings and income targets for owning a home become ever more elusive.

Read more: Head start for home owners makes a big difference for housing stress

So this should mean falling house prices are bad for home owners and good for aspiring home owners, right? In practice, things don't work out quite like this, for several reasons.

Provided they are financially "liquid" (they have a job and can cope financially), home owners have a secret weapon: they don't have to sell.

Research shows housing markets tend to operate in periods of "frenzy" alternating with periods of relative inactivity. Lots of people try to capitalise and trade up in a hot market. Once markets cool, people tend to stay where they are and wait for prices to improve.

For aspiring home owners, this is bad news. Although prices might be falling, fewer people are vacating their houses. This reduces the supply of houses on the market at lower prices.

Weaker markets make loans harder to get

House markets adjust to economic cycles, although these adjustments tend to be exaggerated and are prone to overshooting. The global financial crisis is an obvious example of an extreme correction when asset values plummeted.

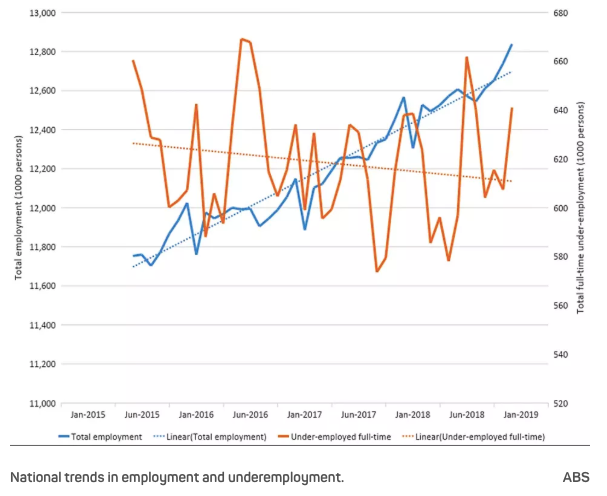

The current dip in house prices in Australia is almost certainly a milder adjustment. However, even minor adjustments in the housing market are associated with adjustments elsewhere in the economy, particularly in labour markets.

The graph below shows the national trends in employment and underemployment over the past three years. Although total employment has been growing, the reported level of underemployment (a measure of the desire of workers to work more hours than they do) was also growing for much of 2018. Low wages growth and limited working hours do not help when people are already struggling to afford a house.

The supply of finance in mortgage markets also depends on the economic cycle. Unfortunately, falling house prices and a deteriorating economic outlook tend to translate to tighter lending conditions.

So while housing prices might be falling in our biggest cities, at the same time it's becoming harder to get a home loan. The number of first home buyer dwellings financed fell by more than 5% in the year to November 2018.

So what's next for the housing market?

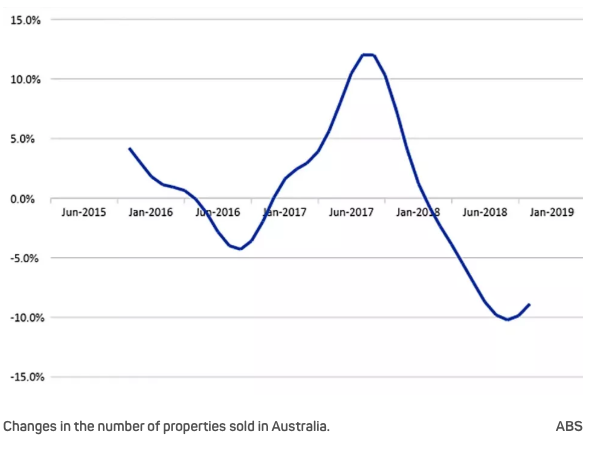

Change in the total number of properties sold is also a useful leading indicator, meaning that transactions data tend to signal a change in market conditions long before average prices begin to change. The chart below shows the year-on-year growth in transactions peaked in the third quarter of 2017.

The growth in transactions began slowing, then became negative in the early months of 2018. These changes occurred much earlier than the plateau, then fall, in prices in late 2018.

The outlook is never certain, but it is worth noting that prices very rarely stabilise or begin growing while the transaction volume is still declining.

Like many sectors of the economy, housing markets are cyclical. But what makes the housing market different is the historical fact that periods of falling prices are much less frequent than periods of rising prices. The market will soon return to its long-run unsustainable trajectory of rising prices and declining affordability.

During the current price adjustment, housing affordability may appear to improve slightly. But low wages growth and limited working hours, coupled with lending restrictions, combine to make it just as hard for first home owners to enter the market.

Read more: Local councils put affordable housing supply in the too hard basket

Current circumstances create opportunity elsewhere in the housing system. In particular, modestly falling prices coupled with lenders issuing fewer mortgages to owner-occupiers create fertile conditions for private residential investors. Times like this tend to favour cash buyers rather than those who need to scrape together a deposit and secure a mortgage before they can buy a house.

Paradoxically, then, declining house prices are no better for housing affordability than rising prices.

Courtey of Author Chris Leishman is a professor of housing economics at the University of Adelaide.

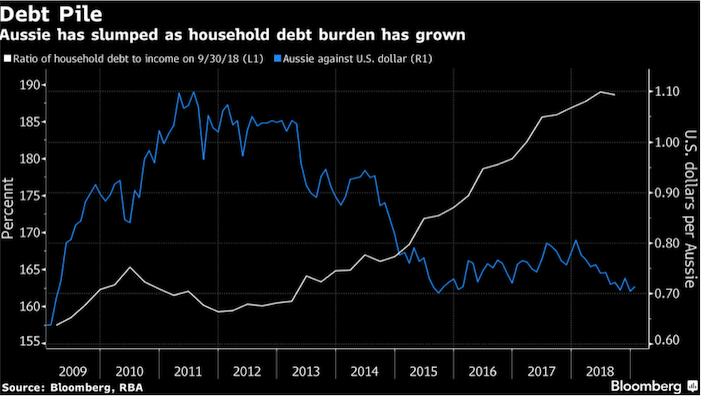

"Debt Threatens to Drag Down Australian Dollar"

By Ruth Carson and Masaki Kondo, January 23, 2019, 2:00 PM EST, updated at January 24, 2019, 2:49 AM EST

The beleaguered Australian dollar faces another threat in addition to slowing global growth and the U.S.-China trade war: an addiction to real estate has created a debt mountain.

After being the worst-performing developed-nation currency in 2018, the Aussie is set to extend losses this year as a near-record level of indebtedness at households make it more likely the Reserve Bank of Australia will cut interest rates to support the economy, according to strategists at HSBC Holdings Plc and Rabobank. HSBC sees a further 7 percent slide to 66 U.S. cents by year-end, while Rabobank tips 68 cents.

"The RBA just sat there watching the housing bubble grow for the past couple of years," said Michael Every, head of Asia financial markets research at Rabobank in Hong Kong. "You're in a doom loop. Now that the Federal Reserve is finally on hold, the RBA can finally talk about cutting again -- and they will."

Australia's household debt-to-income ratio has skyrocketed to 189 percent from 67 percent in the 1990s fueled by low interest rates and an easing of constraints on bank lending, according to data compiled by the RBA.

While the debt ratio edged down in the third quarter as the government sought to restrain lending, it is still almost double the average since the series started in 1977, raising concern over a sliding property market and its impact on the economy. House prices slipped an average 4.8 percent nationwide last year.

Australia's dollar has already tumbled for five straight quarters -- including a decline of 9.7 percent last year. After ending 2019 at 70.49 cents, the Aussie briefly slid to 67.41 cents on Jan. 3 in a so-called "flash crash" when a holiday in Japan led to disjointed Asian markets, the weakest since the global financial crisis in March 2009. The currency was at 70.98 cents in early London trading on Thursday.

HSBC is bearish on the Aussie due to the country's debt binge and also the widening yield discount on Australian bonds compared with U.S. Treasuries, according to David Bloom, global head of foreign-exchange research in London.

"What does concern us about Australia is that their interest rates structure is below that of the U.S., and we would argue that the U.S. is a lower risk profile," he said, referring to Australia's debt levels. "You're getting paid less for the Antipodeans, and you get more risk."

There's a 42 percent chance the Aussie will touch 66 cents by year-end, according to data compiled by Bloomberg based on option prices. A year ago, the same projection for December 2019 had a probability of only 14 percent.

'Keep Cutting'

Rabobank sees the RBA reducing the nation's benchmark rate by another 100 basis points from the already record-low 1.5 percent to help manage the debt burden, Every said.

"When you have an economy that's piling on debt the way Australia does, the currency gets well supported because everything looks fine and dandy in this growth bubble," he said. "And then as soon as you reach the end of the rope, the only thing the RBA can do is cut -- and keep cutting."

While HSBC and Rabobank are both downbeat on the Aussie, the broader market remains positive. The Aussie will strengthen to 74 cents by year-end, according to the median estimate of currency forecasters compiled by Bloomberg.

Morgan Stanley says the Aussie will decline to 67 cents in the second quarter before recovering to end the year at 71.

"Markets are currently pricing in about a 50 percent probability of an RBA rate cut over the next 12 months, fairly reflecting the economic weakness," Morgan Stanley strategists including Hans Redeker in London, wrote in a research note. "Under these dynamics, we see further Australian dollar downside."